When Your Biggest Asset Can't Be Split Evenly

When Your Biggest Asset Can't Be Split Evenly

Not every asset in an estate can be split evenly. Some things — a family business, a piece of real estate, a collection built over a lifetime — carry meaning that doesn't divide neatly. And when the time comes to pass those assets on, the challenge isn't just financial. It's personal.

What is estate equalization?

Estate equalization is a planning strategy that allows families to preserve a meaningful or illiquid asset for the heir who values it most, while ensuring other heirs receive comparable value. Rather than forcing a sale or creating an unequal distribution, the strategy uses financial tools, most commonly life insurance, to create equivalent value for heirs who don't receive the asset itself. The result is an estate plan that is both financially balanced and emotionally thoughtful.

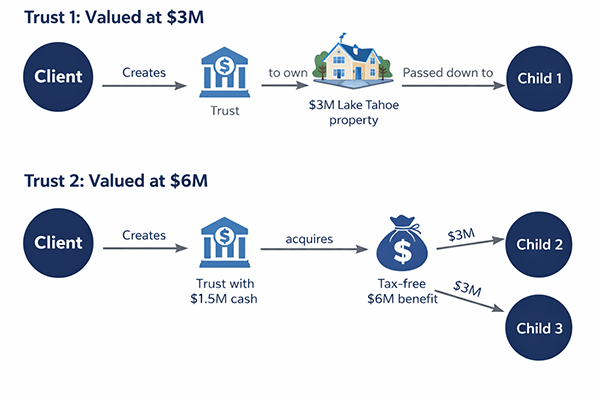

Client story

John and Jane Smith, both age 65, own a $3 million property on Lake Tahoe where their family has gathered for years to ski and vacation. With three adult children and an estate review underway, they faced a question many families eventually confront: how do you pass on something irreplaceable without creating inequity among your heirs?

One child lives nearby and has a deep connection to the property. The other two are on the East Coast and rarely visit. John and Jane wanted to preserve the lake house for the child who would truly cherish it, while treating all three children fairly. Forcing a sale wasn't an option. Leaving the property to one child without addressing the imbalance wasn't either.

The strategy

To keep the property intact, they transferred it into a trust and designated it to the child most connected to it. To equalize the estate's value for the other two, they reallocated $1.5 million of existing family capital to secure a $6 million tax-free life insurance benefit, creating comparable value for the heirs who wouldn't receive the property.

The lake house stays in the family. Every child is treated equitably. And John and Jane's legacy is transferred the way they always intended.

How a two-trust structure creates equitable distribution across all three heirs.

Why trust-owned life insurance works

The vehicle that made this possible is a trust-owned life insurance policy, or TOLI. By holding the policy inside a trust, the death benefit is generally kept outside the taxable estate, meaning more of the family's wealth transfers to the next generation rather than to the IRS. For families with illiquid or emotionally significant assets, TOLI is one of the most efficient equalization tools available. It doesn't require selling anything or asking heirs to agree on valuation.

Is estate equalization right for your family?

These strategies are worth exploring any time a meaningful asset represents a significant or disproportionate share of an estate. The goal isn't just financial parity. It's preserving relationships, honoring intentions, and making sure the people you love aren't left to sort out the complexity on their own.

If your estate includes assets that don't divide easily, we’re here to help. Reach out to our team and let's start the conversation.

Securities offered through Raymond James Financial Services, Inc., Member FINRA/SIPC. This is a hypothetical example for illustration purpose only and does not represent the actual performance of any particular securities or insurance product. Actual investor results will vary. These policies have exclusions and/or limitations. As with most financial decisions, there are expenses associated with the purchase of life insurance and cost can vary with age and other factors. Guarantees are based on the claims paying ability of the insurance company.